Tactical Positioning

On the dawn of some of the most anticipated tariff-related announcements of Donald Trump’s presidency so far, market angst remains elevated. Over the past couple of weeks, we have witnessed significant market movement, with a marked rebound in US Equity implied volatility over the last couple of days. As was the case in the previous bulletin, we remain cautiously constructive on markets and continue to drip feed dry powder into market weakness in keeping with the famous words of Warren Buffet “be greedy when others are fearful.”

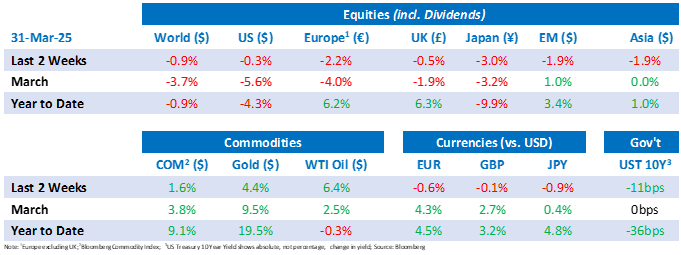

Market Moves

“Liberation Day”

On the 2nd April, the Trump administration will introduce a “reciprocal” tariff policy, aligning US tariffs with those of trading partners while also factoring in what it considers to be non-tariff trade barriers. Officials have, however, emphasised that countries will have the opportunity to negotiate to avoid a full-scale “tariff wall.” Given that previous calculations from the US administration have included taxes such as VAT, alongside more traditional concerns like currency manipulation, the negotiations and final conclusions are likely to remain some way off and market participants need to ready for continued turbulence.

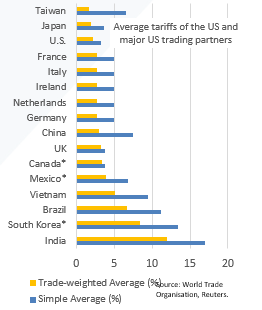

The day will be particularly significant for Trump’s so-called “Dirty 15”—the countries with major trade imbalances with the US. Last year, according to federal census data, the US had its biggest trade deficits with China, the European Union, Mexico, Vietnam, Taiwan, Japan, South Korea and Canada.

The table on the below highlights the average tariffs imposed by the US and its 15 largest trading partners. Countries with existing Free Trade Agreements are marked with an asterisk (*), though these agreements have offered little protection for these nations so far.

With negotiations still on the table and mixed signals on the severity of forthcoming measures, the market is yet to find any consensus. A softening in rhetoric early last week fuelled a partial US market recovery, but this was swiftly quelled by Trump’s announcement of 25% tariffs on all car imports and expressing little to no concern for rising prices. Trump has framed 2nd April as America’s “Liberation Day” but perhaps the markets’ Judgement Day would be more fitting.

We will be monitoring the news flow closely, with both eyes on any market responses, and are looking at our dollar exposure given the US Presidential team’s desire to devalue the currency.

The German debt accelerator

While tariffs will be a key concern for Europeans, there has been a major development on the fiscal front. Germany’s CDU, SPD, and Greens have successfully cleared the Bundestag hurdle, securing the two-thirds majority required to amend the country’s debt brake. This marks a shift for traditionally debt-averse Germany and could have far-reaching implications for Europe—especially as Russia’s invasion of Ukraine continues, the planned ceasefire disappointments and US President Donald Trump continues to pull back on US support for NATO and the defence of Europe.

The reforms rest on three key pillars. First, defence spending above 1% of GDP would be exempt from fiscal rules, effectively lifting borrowing constraints for major military expenditures. Second, the establishment of a €500bn (12% of GDP) deficit-financed infrastructure fund, with spending spread over a decade. Third, federal states would be allowed to run small deficits.

Given the structure of these reforms, estimating the precise scale of the fiscal expansion is challenging: Capital Economics projects it will be around 1-2% of GDP. If accurate, this would push the budget deficit to approximately 4.5% of GDP.

Much of this news appears to have already been priced, given German and European (ex UK) equity market returns of c.12% and c.9% so far this year. 10-year German government bond yields have also fallen by more than 10bps since our last bulletin.

UK Spring Statement

The UK government’s Office for Budget Responsibility revised its 2025 UK growth forecast from 2% at the Autumn Budget, widely condemned as optimistic at the time, down to 1% while growth in future years was revised marginally upwards. The likelihood of government borrowing overshooting expectations in 2025 and breaching the government’s own fiscal rules led to Rachel Reeves announcing welfare spending cuts of £4.8bn alongside reforms to public services. This was not sufficient to reassure the market completely and despite a soft inflation number the UK 10-year gilt yield has risen slightly over the past two weeks.

Türkiye troubles

The news flow has recently intensified in Türkiye with opposition leader, and Istanbul mayor, Ekrem Imamoglu jailed on corruption charges. Huge public demonstrations followed given the seemingly increasing authoritarian direction. The Turkish equity market fell more than 15% and the central bank hiked overnight lending rates by 200bps to 46%.

ECONOMIC UPDATE and central bank indecisions

As expected, the Federal Reserve (“FED”) pause on rate cuts continued, but with more indications that rates may be cut in future than at previous meetings. FED Chair, Jerome Powell, said that they had “seen some signs of increased tightness in money markets” suggesting scope for future rate cuts. The FED also announced a slowing in the pace of Monetary quantitative tightening, with the reduction in Treasury holdings to slow from $25bn to $5bn a month from April 1st. The Bank of England also held rates, in line with expectations, citing an uncertain policy environment.

On the data front, US GDP was 2.4% higher in Q4 2024 than the same quarter the previous year, above expectations of 2.3%, while annual Core Personal Consumption Expenditure inflation marginally surprised to the upside at 2.8%. US Retail sales were below expectations, up just 0.2% for the month (0.6% expected), whilst the labor market held up well with Continuing and Initial Jobless Claims roughly flat on the previous month (223k/224k). US Conference Board Consumer Confidence came in lower than expected at 92.9, a level not seen since February 2021.

Download the bulletin here.