Tactical Positioning

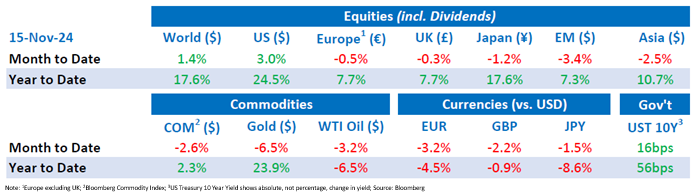

Market Moves

Red sweep victory

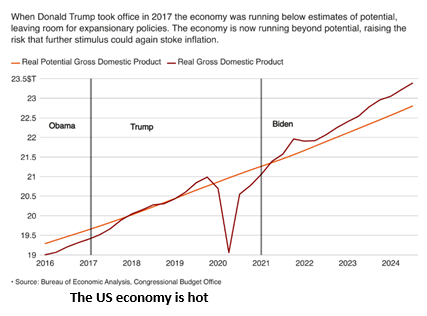

Trump’s victory in becoming the 47th President of the United States marks an historic comeback. Addressing supporters, Trump predicted a “golden age” for the United States, arguing that America had given the Republican Party a powerful mandate. The Republican Party’s control of the White House and both houses of Congress will provide them with greater leeway to implement their agenda. This will have major implications for US trade, fiscal, immigration, climate change, and foreign policies. Trump’s proposed trade tariffs are designed to boost domestic production at home but could spark reactionary policies against the US and issues with supply chains. His pledges to reduce corporate taxes and implement new tax cuts could boost growth but will also increase US debt and exert upward pressure on inflation.

Trump’s comeback sent global markets into a frenzy as they scrambled to price in a new regime for the world’s largest economy. Wall Street stocks hit a record high with a broad-based equity rally as investors expected a faster-growing US economy from the president-elect’s plans, which would benefit a wider range of sectors beyond highly valued mega-cap tech stocks. The dollar index, a measure of the currency against a basket of rivals, rose by 1.6%, marking its biggest one-day gain in two years. Bond prices fell to reflect concerns that interest rates may not fall as quickly if the economy is strong, while commodity prices fell as investors anticipate that higher tariffs might hinder global growth. European and Chinese stocks fell as Trump’s proposed tariff policies threaten their exports and economic growth.

Clouded monetary policy

The Federal Reserve (“Fed”) cut its benchmark interest rate by 25 basis points to 4.5-4.75%, two days after the election result. Fed Chair Jerome Powell stated that the risks to achieving both stable inflation and a healthy job market are now roughly balanced. While expectations of further rate cuts are clouded by potential upward pressure on growth and consumer prices from Trump’s economic agenda, Powell declined to speculate on how the new US administration might impact monetary policy. There are concerns that the Fed’s independence could be in jeopardy given Trump’s previous consideration of removing Powell as Chair and the new President’s desire for greater influence over monetary policy. Powell has confirmed he will not step down early.

The release of the US Consumer Price Index (“CPI”) data, which rose in line with expectations to 2.6% year-over-year in October, led to a relief rally in bonds as it increased expectations of an additional quarter-point cut at the next Fed meeting to an 82.5% chance. The “core” CPI, which excludes volatile food and energy prices, held steady at 3.3% on an annual basis. A subsequent comment from Powell, reaffirming that the Fed is in no rush to cut rates, brought the odds of a December cut down to 61.9%.

US outperformance widens

The decline in European equities following the US election results has caused European markets to lag behind the US market by a record margin. While US stocks have surged by 24.6% this year, European stocks have risen by less than 10%. The euro has fallen to a one-year low of around $1.05, as investors anticipate slower growth in Europe and more interest rate cuts by the European Central Bank. Since the financial crisis, the US, driven by the rise of tech giants, has performed significantly better than Europe which is still dominated by banking, energy, consumer and industrial sectors.

Economic Updates

Eurozone GDP grew by 0.4% in the third quarter, sustaining hopes for a soft economic landing. The European Commission forecasts 0.8% growth for 2024, though Germany is expected to contract by 0.1%. Employment rose by 0.2% in the third quarter, following a 0.1% increase in the previous three months.

The UK economy slowed in the third quarter, with GDP up 0.1%, down from an increase of 0.5% in the previous quarter. A 0.1% contraction in September, largely driven by weaker manufacturing, contributed to this slowdown. Annual wage growth excluding bonuses averaged 4.8%, the lowest in over two years.

In China CPI rose slightly less than expected at 0.3% year-on-year in October, driven mainly by lower food and energy prices, whilst core inflation increased by 0.2%. The producer price index fell 2.9%, continuing deflation in factory gate prices since late 2022. Retail sales rose 4.8% year-on-year, exceeding expectations.

Download the bulletin here.