Tactical Positioning

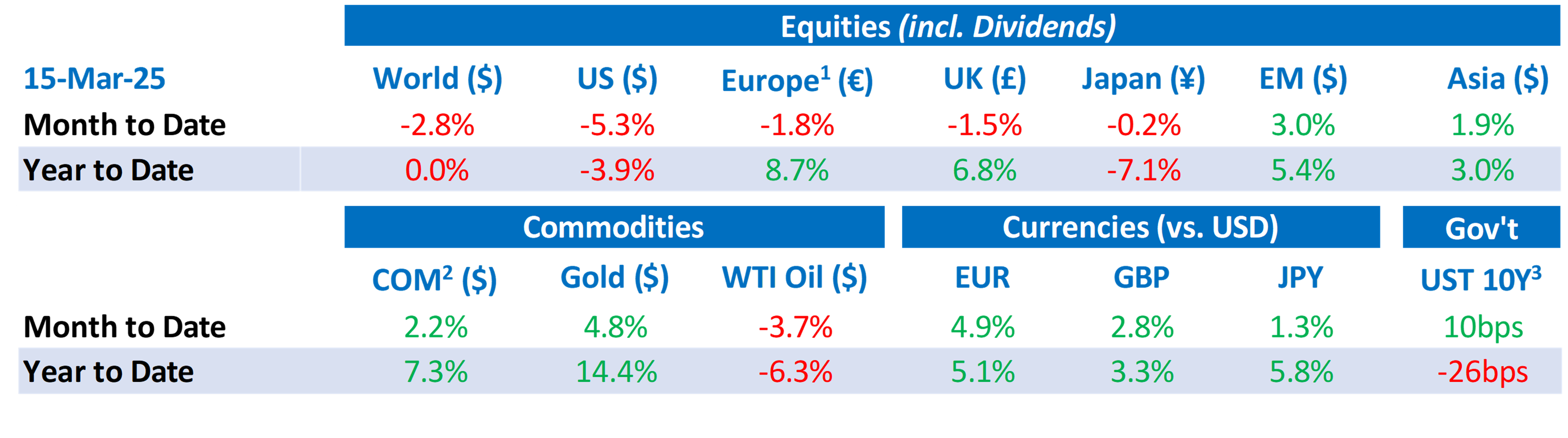

Market Moves

Tariffs…20%, 25%, 50%, 200%

President Trump has so far imposed a 20% levy on Chinese goods, 25% tariffs on all steel and aluminium imports and 25% tariffs on many other imports from Mexico and Canada. Following the introduction of new US tariffs on EU metal imports, the European Commission initiated raising tariffs on US imports valued at up to €26 billion which could include a 50% tariff on US whiskey (bourbon). In response the American president has threatened a 200% tariff on any alcohol coming to the US from the EU. The tariff war will not end here.

Despite sharp market declines and mounting recession fears, Commerce Secretary Howard Lutnick defended the tariff policy as essential to revitalizing domestic manufacturing. However, the economic fallout has been significant. US manufacturers relying on imported raw materials now face rising input costs which may squeeze profit margins and/or drive consumer prices higher. The prospect of this has contributed to a slowdown in industrial output and weakened the outlook for economic growth. Financial market volatility has increased, particularly in sectors deeply embedded in global supply chains — including cars and technology. Analysts caution that if the trade disputes persist, the uncertainty could weigh heavily on business confidence and capital expenditure plans, risking a deeper economic contraction. JP Morgan’s Chief Economist believes that the risk of the US slipping into a recession this year has increased to 40%.

War in Europe

Trump has threatened Russia with severe financial sanctions if it refuses a 30-day ceasefire, but in Europe this threat is seen as ineffective and more a form of diplomatic pressure than genuine support for Kyiv. The US president’s adoption of a more conciliatory stance toward Russia has led to many European nations including the UK to announce an increase in planned spending on defence. In Germany, Friedrich Merz the chancellor-in-waiting has succeeded in persuading the Green party to support an amendment to the country’s constitution to allow a larger budget deficit to fund defence spending.

Magnificent or Maleficent

The renamed “Maleficent 7” — Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia, and Tesla — spearheaded market gains throughout 2024, fuelled by the AI boom. However, since their peak in February 2025, these tech giants have collectively lost approximately $2.7 trillion in market capitalization and led a broader market downturn. The group has declined 14% from its peak, more than twice the fall of the average of the next largest 493 companies. The combination of declining earnings forecasts, tighter profit margins, and geopolitical instability has led analysts to question whether these former market leaders will continue to justify their premium valuations.

A time to sell, a time to buy

The US stock market has experienced a sharp correction, shedding nearly 10% from its recent peak — marking the steepest decline since 2022. The index has also fallen below its 200-day moving average for the first time since October 2023. Some investors believe that if prices do not recover back above this level in the near future then we may see a more sustained downturn. This may present a buying opportunity but as is often the case it is difficult to know how long or how deep the setback will be and therefore when investors should start buying again. Now that the pullback has arrived, uncertainty clouds the opportunity. Goldman Sachs has revised its 2025 equity market outlook, cutting its forecast for how much the market will rise this year from 10.5% to 5%, citing a combination of slower economic momentum and rising geopolitical risks.

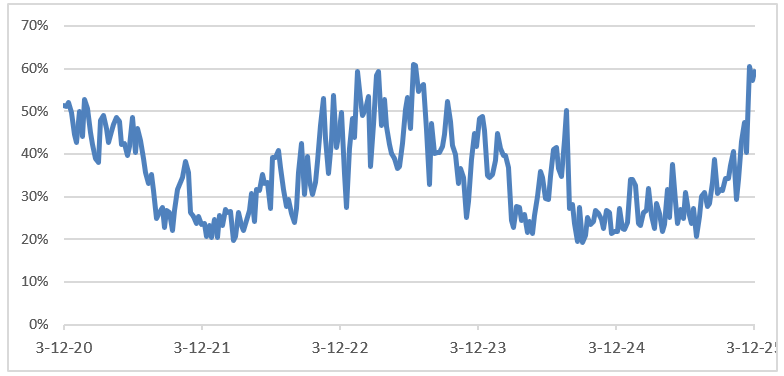

The latest American Association of Individual Investors (“AAII”) sentiment surveys show that individual investors have recently reached the highest level of bearishness since October 2022. When sentiment is this bearish it is normally viewed as a contrarian signal — meaning that when everyone is pessimistic, a recovery may be on the horizon, as the bad news is already “priced in.”

Economic Updates

US inflation fell to 2.8% in February down from 3.0% the previous month whilst the economy added 151,000 jobs although unemployment rose by 0.1% to 4.1%.