Tactical Positioning

Market Moves

US Jobs better than expected

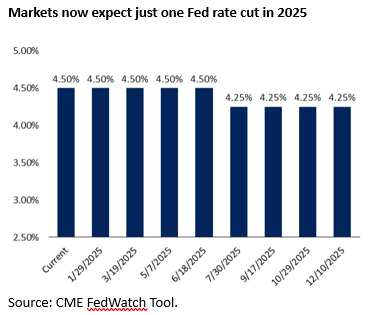

A better than expected US jobs report surprised markets on 10th January, suggesting that the US economy and labour market may be more robust than anticipated. The Labor department reported that non-farm payrolls grew by 256,000 in December, up from 212,000 in November and well above expectations of 165,000. The unemployment rate also edged down to 4.1% from 4.2% beating expectations. This better than expected data has led to a sharp reversal of the expected Federal Reserve (“Fed”) rate cuts for the year with Wall Street now pricing in just one cut of 25 basis points this year. Some analysts, including those at Bank of America, warning that the Fed’s cutting cycle may have ended. Treasury yields have moved sharply higher in response to the prospect of higher for longer rates, fuelled by the recent jobs report and anticipated fiscal policy shifts from the incoming presidential administration. The 10-year yield has risen to its highest level since November 2023.

2025 starts with a rally

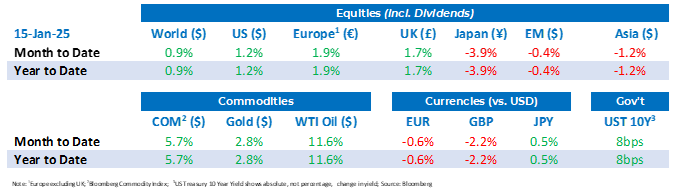

Equity markets have started the year with positive momentum. Sentiment in US equity markets has recently shifted between optimism surrounding anticipated tax cuts, tariffs, deregulation, and immigration reforms following Mr. Trump’s election victory and concerns that inflation remains too high leading to the likelihood of prolonged higher interest rates. This has led to the increase in bond yields which in turn may impact equity markets, particularly more growth-oriented stocks which can be more sensitive to interest rates.

Dollar dominance

The US Dollar Index (calculated against a basket of currencies) has risen 9% since the end of September as investors adjust expectations to reflect fewer rate cuts by the Fed. For UK and European investors with US exposure, the stronger dollar has benefitted returns in sterling or euro terms, however the stronger dollar also reflects higher interest rates, which have weighed on equity valuations. Additionally weak UK and Eurozone manufacturing data and the threat of higher natural gas prices has put downward pressure on sterling and the euro. Elsewhere, the impact of the strong dollar can be seen across emerging markets, which are down 0.4% in dollar terms since the start of the year. The strong dollar adds strain to emerging markets by increasing the cost of dollar-denominated debt and potentially triggering capital outflows.

Reeves under pressure

Although bond prices have weakened globally, the UK Gilt market has experienced its own pressures in recent months. The UK Chancellor, Rachel Reeves, has recently faced criticism of her economic plan in the wake of high borrowing costs, rising yields and the threat of stagflation. There are also concerns that the heavy borrowing requirement, low growth and sticky inflation could force the government into raising taxes or cutting spending. Nevertheless, there was some relief from the lower than expected UK CPI release of 2.5%, which has fallen 0.1% from November 2024. Overall, the UK 7-10 year Gilt index has fallen close to 2.0% since the start of the year

Economic Updates

The December headline US Consumer Price Index (CPI) came in as expected with a 2.9% rise, up from 2.7% in November 2024. Earnings season has opened to a strong start with US banks JPMorgan Chase, Goldman Sachs and Citigroup posting strong rises in profits at the end of last year, powered by a boom in trading and dealmaking.

In Europe, Germany’s industrial production for November came in below expectations, falling 0.5% month-on-month, signalling ongoing weakness in the region’s economy. Lastly, China’s trade data showed increased momentum in December, with exports growing by 10.7% year-on-year compared with 6.7% in November.

Download the bulletin here.