Tactical Positioning

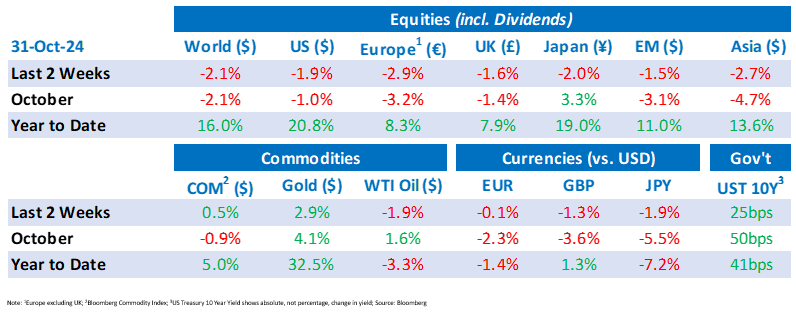

Market Moves

Q3 Earnings – negative on tech

Third-quarter earnings reports from US companies started last week with mixed results, particularly among major tech firms. Microsoft shares dropped 6% on weaker-than-expected cloud revenue forecasts and Apple’s shares declined nearly 2% in after-hours trading, as it projected slower sales growth of “low-to-middle single digits”, below analysts’ expectations of 7%. Meta, Facebook’s parent company, fell over 4% after reporting lower-than-expected user growth and cautioning about increased capital expenditure for 2025. In contrast, Alphabet, Google’s parent, rose following strong revenue growth.

UK budget digest

On Thursday markets reacted to the additional borrowing announced in the UK Budget. Specifically, the spread between 10-year gilt yields and German bunds widened by 9.4 basis points, reaching 206 bps — its largest gap since October 2022, during Liz Truss’s term. Chancellor Rachel Reeves announced £40 billion in tax hikes, primarily through an increase in employers National Insurance, with changes to capital gains and other taxes being less significant than expected. Sterling fell by around half a percent against the US dollar to $1.2899, making it the worst-performing G10 currency that day. Additionally, investor expectations for the extent of UK interest rate cuts by June 2025 dropped from 86 bps on Wednesday to 80 bps by Thursday’s close.

Bond yields take the high road

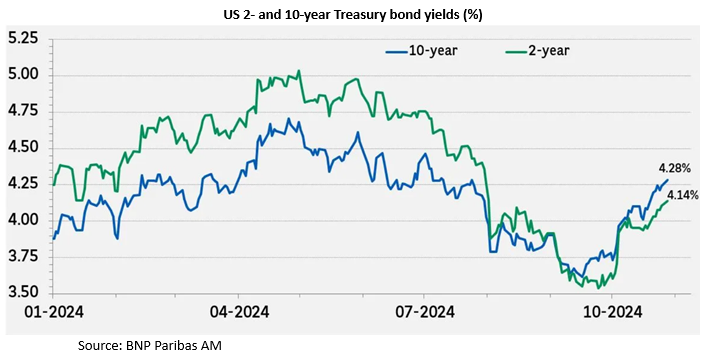

Yields on US Treasury bonds rose, signalling (either or both) the ongoing resilience of the US economy and expectations for increased bond issuance to cover growing deficits. Investor sentiment has shifted: whereas investors may have once overestimated potential rate cuts by the Fed, the on-going strength of the economy now leads some to expect a slower pace of interest cuts. This evolving outlook reflects heightened awareness of the Fed’s balancing act between sustaining economic growth and managing inflationary pressures.

According to the Bureau of Economic analysis, US GDP (“Gross Domestic Product”) grew 2.8% in the third quarter, underscoring the strength of the US economy despite relatively high interest rates. This economic resilience paired with concerns that, whoever wins the election, Federal borrowing will continue increasing contributed to a sell-off in US Treasuries. The 10-year yield has risen from around 3.7% to 4.25% in the past four weeks. Meanwhile, markets are still anticipating a 0.25% rate cut at each of the Federal Reserve’s remaining two policy meetings this year.

US Treasury yields could rise further but are unlikely to exceed 2023 highs. Inflation is expected to reach the Fed’s 2% target in the coming months as wage and housing inflation cool. A « soft landing » is the base-case economic scenario among commentators, suggesting growth will slow without a recession, allowing the Fed to ease policy gradually.

Gold Rush

Gold has been the unsung hero of 2024 (so far). The safe-haven asset has risen 38% this year reaching a new all-time high on 30th October of $2,785 per ounce. Silver, historically more volatile than gold, has risen 44% since the turn of the year. The rise in gold has reflected geopolitical concerns, which has lead to increased demand by central banks and private investors seeking protection against inflation and external controls.

Economic Updates

In contrast to the strong GDP growth seen stateside, German GDP fell 0.2% in the third quarter although Eurozone GDP increased 0.9% (vs 0.6% expected) and annual headline inflation in Germany ticked up to 2% in October from 1.6% in September. In October, economic activity looked weak according to the Purchasing Managers Index (“PMI”) figure which rose marginally to 49.7 from 49.6 the previous month (a reading below 50 is indicative of falling demand) raising concerns about the outlook for the European labour market.

In the US, October Services and Manufacturing PMIs both came in above expectations at 55.3 and 47.8 respectively. The latest initial jobless claims were slightly below expectations (216K vs 228K expected) although US Nonfarm Payroll growth came in below expectations at 12K vs 106K expected.

Download the bulletin here.