Tactical Positioning

With the US equity market back at all time highs, a consolidation phase could now be expected. President Trump’s restless policymaking has a habit of creating questions rather than providing immediate answers and the mixture of tariff changes, Ukraine/Russia negotiations and the seemingly endless Executive Orders suggests to us that investors should take a pause before committing further capital. A period of ‘digestion’ seems in order.

Market Moves

Tariff mania

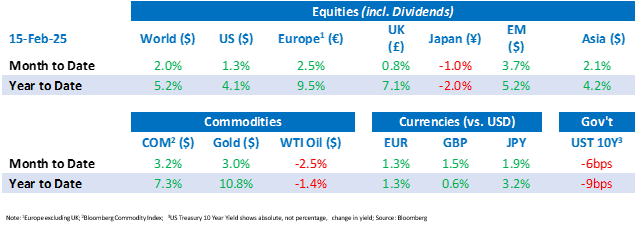

Tariff news dominated headlines over the fortnight with President Trump signing executive orders to impose a 25% tax on all imports from Canada and Mexico, before suspending the decision for a month after the neighbouring Countries agreed to improve their border security in a bid to curb the smuggling of fentanyl. The White House then announced 10% additional tariffs on all Chinese imports, following which China responded with a flurry of retaliatory tariffs to the tune of 15% on some American goods, including coal, liquified natural gas and agricultural machinery. Amidst the turmoil US equities finished the midway point in February in positive territory, +1.3%.

A fresh swathe of tariffs was declared later in the fortnight, with Trump maintaining a 25% tariff on all steel imported into the US and a 10% tariff on imports of aluminium, hitting the likes of China, Canada, the UAE and Mexico the hardest. The tariffs will come into effect from 12th March.

Make Europe Great Again

As mentioned in our previous Bulletin, European stocks have lagged their American counterparts for a decade but have enjoyed their best start to a year since 2000. Europe’s main stock index, hit an all-time high during the fortnight, as did Germany equites, whilst the UK has moved up 7.1% in 2025. Investors have piled into European equities buoyed with enthusiasm surrounding undervalued assets, the prospect of loose monetary policy from the European Central Bank (“ECB”), and a rotation away from technology stocks.

US CPI

Annual headline US inflation, as measured by the Consumer Price Index (“CPI”), unexpectedly increased in January to 3.0%, marginally ahead of analysts’ projections of 2.9% and reducing the prospect of additional rate cuts for the rest of the year. One notable contributor to the rise was the price of eggs, which shot up 15.2% over the month owing to avian flu. Core CPI, which excludes the volatile effects of energy and food prices, was also higher than expectations at 3.3%, above the December rate of 3.2%. The release provoked instant unease in the bond market with government bonds selling off as investors digested the prospect of a ‘higher for longer’ environment. US equities also fell on the news, but managed to pare back much of the daily losses by the market close. Whilst the FED does not appear to be in any hurry to cut rates, President Trump was quick to share his thoughts via his Social Media platform, Truth Social, exclaiming “Interest Rates should be lowered, something which would go hand in hand with upcoming Tariffs!!!”.

Under a cloud

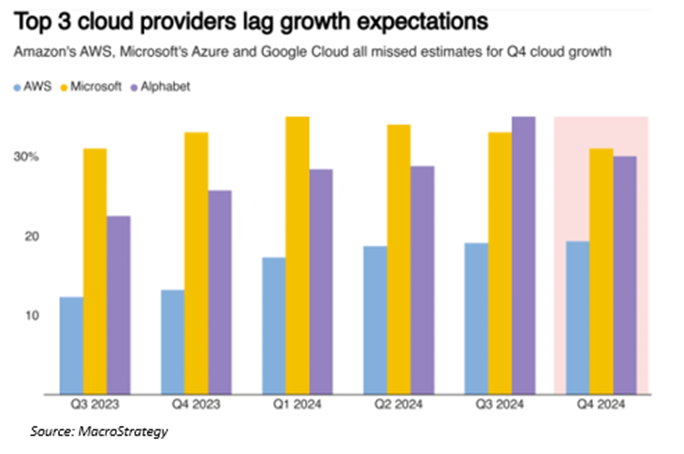

Alphabet, Google’s parent company, did little to impress investors with their fourth quarter earnings release. Despite improving sales, operating margins and better-than-expected profit, annual revenue growth from its Cloud business decelerated by 30%. Capital expenditure into Artificial Intelligence (“AI”) was also expected to hit an eye-watering $75bn over 2025, well ahead of Wall Street’s expectations of $58bn. Google’s share price fell 9% after hours. In a similar vein, Amazon showcased impressive growth in their overall revenue and profits, but also warned of slowing growth ahead for their cloud computing arm, Amazon Web Services. Perceived overspending (of approx. $100bn) on AI, also contributed to the stock falling close to 3% on the news.

UK not OK?

The Bank of England (“BoE”) cut interest rates by 25bps from 4.75% to 4.5%, down to its lowest level in 18 months. Whilst the decision was broadly expected, the 9 voting members of the Monetary Policy Committee (“MPC”) were split 7-2, with the 2 dissenters opting for a slightly higher cut of 50bps. UK equities rose on the news. Despite this, the BoE released fresh economic forecasts projecting UK inflation would soar to 3.7%, nearly double the Bank’s 2% target, largely owing to the rise in employers’ national insurance contributions and natural gas prices hitting two-year highs. A further blow was the downgrade of the UK’s growth forecast for the year, which was slashed from 1.5% to a lacklustre 0.75%, painting a bleak stagflationary outlook for 2025 and highlighting the scale of the challenge ahead for UK Chancellor Rachel Reeves. The path for future cuts remains murky, but markets are currently pricing two additional cuts in 2025.

Economic Updates

Following the hotter than expected CPI print, US Producer Price Index (“PPI”) data also came out higher than expected (+0.4% for the month versus the estimated +0.3%), although some of the underlying components were slightly softer.