Tactical Positioning

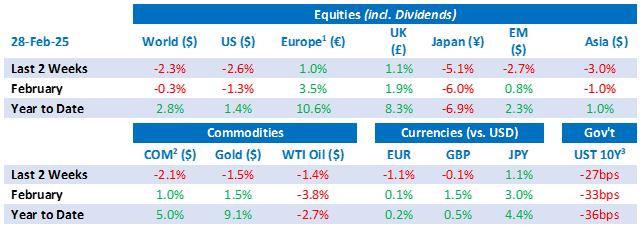

Market Moves

The T words

Trump, tariffs, maybe even trade: Market headlines follow a certain degree of alliteration, but whereas in the past investors could reasonably ignore the tariff threats of the US President, this is no longer the case. The global equity market is flat in US dollar terms since Trump assumed office, having given back earlier gains over the course of the last two weeks. Market volatility is centred around messaging coming out of The Oval Office. At the time of writing, and with a degree of trepidation, knowing that the narrative can change at any moment, the tariffs are back on. In specific terms, this means an additional 10% for China, and the implementation of sweeping 25% tariffs on goods from Mexico and Canada, due to come into effect on Tuesday 4th March. If enacted, this will likely have knock-on effects for price levels, consumption and the broader macroeconomic environment.

Zelenskyy and Trump clash in the White House

When Volodymyr Zelenskyy, Donald Trump and JD Vance met on Friday to discuss a potential mineral rights deal, very few predicted it would end the way it did. With raised voices and ‘disrespect’ derailing the talks, the joint press conference was hastily cancelled, and the Ukrainian delegation was sent packing under the instruction not to return until it is ‘ready for Peace’. This leaves Ukraine and the rest of Europe in a quandary, amid the realisation that they may soon be responsible for their own security. One area of the market which is flourishing, perhaps unsurprisingly, under this backdrop is European defence stocks. Rheinmetall (+38% in February) and Leonardo (+31% in February) being two good examples of companies benefitting from the Russia-Ukraine conflict and prolonged uncertainty around the US’s commitment to Europe. With defence spending increasing across the board and tariffs looming, the natural inclination will be for European governments to favour their own industries over American equivalents.

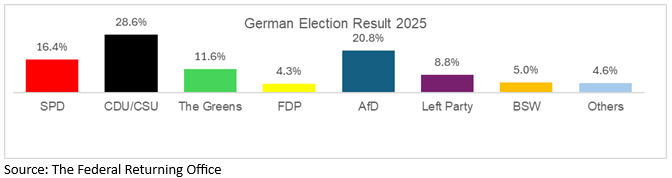

German election

Turnout was high and Friedrich Merz’s Christian Democrats (CDU) secured victory in Germany’s election. Much of the talk leading up to voting focused around loosening the ‘debt brake’, which keeps the German fiscal deficit limited to 0.35% of GDP as opposed to 3% for other members of the EU. The race is now on to form a coalition government before the Easter deadline set by Merz. To loosen the spending rule, a constitutional change is necessary and that requires a two-thirds parliamentary majority. With differing political priorities amongst the other parties and the exclusion of second placed far-right party Alternative for Germany (AfD) from talks, this will not be easy to achieve. From a market perspective, a loosening of fiscal policy and increased investment by the German government should boost German growth and equities but may result in a downward pricing of German Bunds.

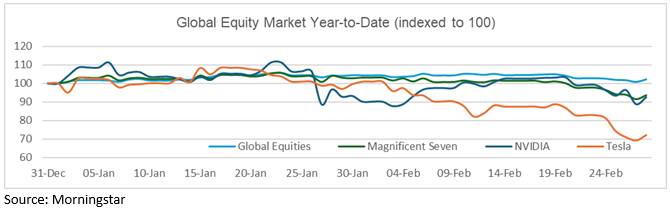

NVIDIA earnings and the ‘Sad Seven’

You know markets are struggling to move higher, when not even NVIDIA can save the day. The US-based chipmaker reported fourth quarter earnings last week and despite the headline revenue figures topping analyst estimates it was concerns around the gross margin number that sent the stock tumbling (down 8.5% on the trading session). Tesla, another of the magnificent cohort, has also been unravelling. After a stellar fourth quarter, Tesla is down 28% this year as Elon Musk’s political involvement is seen as a risk on both his time management and brand perception amongst primarily liberal Tesla drivers. This means that the ‘Magnificent Seven’, including Tesla and NVIDIA, have underperformed the broader global indices by around 10% so far this year.

How much was your coffee?

If your plan was to watch the latest geopolitical events unfold with a cup of coffee in hand, you may want to check the price first. Despite slightly coming off its early-February highs, coffee bean prices are 95% higher than a year ago. Disappointing harvests in Brazil and Vietnam due to droughts and extreme weather in 2024 are mainly to blame.

Economic Updates

UK CPI data for January surprised on the upside at 3.0%, against consensus estimates of 2.8% with transport costs notably higher (air fares and motor fuel). Weak economic data in the US sparked market volatility on the 21st February as manufacturing and consumer sentiment data dropped sharply indicating near stagnation. US Core PCE inflation came in at 2.6%, down from 2.9% the previous month in line with expectations.

Download the bulletin here.