Tactical Positioning

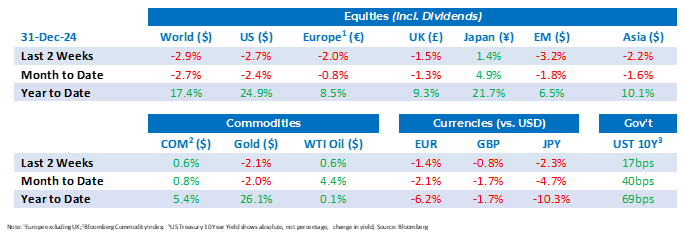

The numbers below show a difficult end to an otherwise robust year for equity markets. After two consecutive 20%+ years of performance from US equities we would be cautious of forecasting anything similar in 2025. It has been more than 25 years since US equities managed 3 years of 20%+ returns. That said, analysts are forecasting 15% earnings growth for the top 500 US companies in 2025 with falling interest rates providing an attractive backdrop. In these circumstances it could be wrong to be too cautious and we intend to keep our exposure to US equities relatively high for the foreseeable future.

Market Moves

2024 was another strong year for equities, with major indices posting solid returns. However, the year also brought volatility, as rate cuts came more slowly than anticipated, geopolitical events sparked investor concerns, and the summer saw significant market turmoil and unlike 2023 there was greater variability in performance across asset classes

The US leads gains

US economic growth exceeded expectations in 2024 and the Federal Reserve (“Fed”) started to reduce interest rates. This led to the S&P 500 posting a total return of +25%, which secured its biggest two-year gain since 1998. Much like 2023, most of the index gain was powered by strong performance by the Magnificent 7, which were up 67% in aggregate. Fundamental company performance remained the key driver of these returns.

In its final meeting of 2024, the Fed surprised markets with a hawkish stance in its updated economic projection. While rates were cut by 0.25%, bringing the fed funds rate to 4.25-4.5%, the dot plot of members expectations indicated only two rate cuts in 2025, a notable contrast to the September estimate of four. Markets initially reacted by moving sharply lower, but the last full week of the year saw major indices deliver moderate gains, extending the December rally before pulling back as markets closed for Christmas. The rally was driven predominantly by large-cap growth stocks, with technology-focused companies leading the charge, underscoring the trend of US large-cap equities as the clear standout for the year. Despite expectations of negative earnings growth, small and medium sized companies posted a solid gain of 12.2% over the year, buoyed by recent optimism surrounding deregulation and corporate tax cuts.

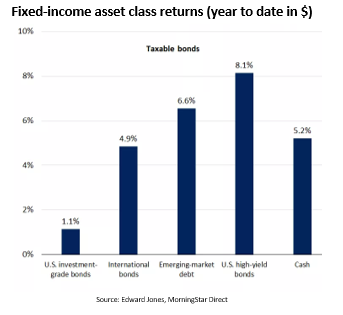

A diversified year for fixed income

In 2024, the importance of bond diversification became clear, as returns differed significantly across sub-asset classes. For example, despite offering lower yields, international bonds significantly outperformed US investment grade.

Even though the Fed’s rate cuts lowered short-term rates, cash posted its highest return since 2000 and has outperformed US investment grade bonds for the third time in the past four years. Looking ahead, cash returns are expected to be more modest as the Fed continues its gradual easing cycle.

A record year for Bitcoin

The price of Bitcoin, the most widely known cryptocurrency, more than doubled to over $100,000 in 2024. Sentiment was boosted by the approval of Bitcoin exchange traded funds (“ETF”) in the US. BlackRock’s Bitcoin ETF surpassed industry records and in just 11 months grew to over $50 billion in assets. Another supportive factor was Donald Trump’s election victory and hope for his crypto-supportive policies.

Demand for Bitcoin is based on investor belief in its potential to be more widely adopted, but it remains highly volatile and its value could tumble if it’s not widely adopted. We continue to monitor it closely.

Economic Updates

The Conference Board US consumer confidence index fell in December from 112.8 in November to 104.7. Most notably, the expectations component of the index—which measures consumers’ short-term outlook for income, business, and labor market conditions—saw the sharpest drop, falling 12.6 points to 81.1. A reading below 80 can serve as a signal for an upcoming recession.

The US Labor Department reported applications for unemployment benefits declined slightly to 219,000 for the week ended December 21. However, continuing claims rose to 1.91 million for the prior week, the highest since late 2021, suggesting that it is taking longer for out-of-work individuals to find new jobs.

In the UK, the most notable data came from the Office for National Statistics, which lowered its final estimate for third-quarter economic growth to 0.0% from 0.1% and its estimate for Q2 growth to 0.4% from 0.5%, adding to worries that the economy has stalled.

Download the bulletin here.