Tactical Positioning

We finish the year with a full weighting in equities and bonds and a positive outlook into the early months of 2025. In our first Bulletin of 2024 we wrote that a full weighting in bonds and equities was justified and that ‘buying the dips’ was back on the cards. This stance has been maintained across the year and has delivered positive performance aided by our preference for high relative US equity exposure and a bias for growth type companies. As we look into 2025, we may make adjustments but our long-term focus on US equities is unlikely to fade. A flexible labour force and low taxation system combined with the abundant availability of credit puts the US in a special place in the world when it comes to growth opportunities.

Market Moves

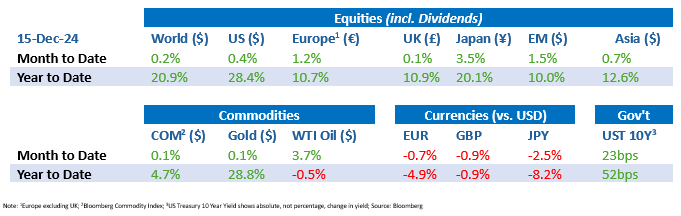

Interest rates falling and expect more cuts in 2025

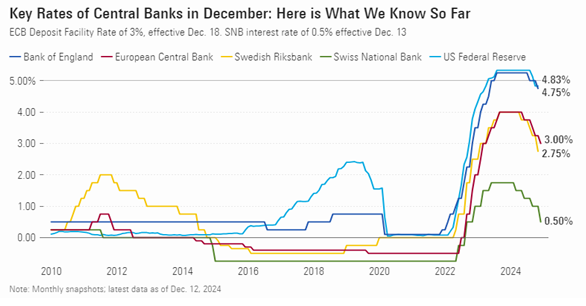

The likelihood of lower interest rates continues to support bond markets. The European Central Bank (“ECB”) cut rates by 25bps from 3.25% to 3% on 12 December in order to support weak economic growth and the Swiss National Bank cut rates by 50bps on the same day to 0.5%.

In the US, the Federal Reserve (“Fed”) is likely to make another four or five 25 basis point interest rate cuts in the next twelve months with the next possibly at its meeting tomorrow. In the UK, where inflation expectations have risen, in part owing to the increase in the employment tax levied on companies employing staff in the UK, the Bank of England is likely to remain cautious when it meets on Thursday and hold interest rates at current levels.

Political shenanigans

For the first time in weeks political uncertainties in Europe and Asia seemed to receive more news coverage than announcements by president-elect Donald Trump. In South Korea, the Korean won weakened and the stock market initially fell on the back of President Yoon Suk Yeol’s declaration of martial law and the subsequent widespread demonstrations. The decision was subsequently reversed and on 14th December, the National Assembly voted for Yoon’s impeachment. The won and Korean equity market have since recovered most of their falls.

In France Michel Barnier lost a no-confidence vote in the National Assembly triggered by his austerity budget involving tax hikes and spending cuts. He was replaced by François Bayrou on 13th December and is the shortest serving French prime minister, having remained in power for three months. The European Union (“EU”) expects the French government deficit to reach more than double the EU limit at 6.2% of gross domestic product (“GDP”) this year.

President Bashar al-Assad of Syria fled Damascus ending his 14-year administration and the end of a 50-year family dynasty. Although Syria is not a major player in the oil industry, its location amongst significant oil producers in the Middle East and its relationship with Russia and Iran could affect the market. According to Reuters in the immediate aftermath of Assad’s departure, oil prices increased by around 1% with Brent crude at $72.14 per barrel and US West Texas Intermediate crude at $68.37.

Healthcare Reckoning

In the US fears of increased regulations in the healthcare sector and the assassination of United Health’s chief executive, Brian Thompson led to weakness in the share price of many healthcare companies. Senator Elizabeth Warren and Senator Josh Hawley introduced a bipartisan bill to create pharmacy benefit manager control legislation on 11th December. If passed, the legislation would break up some of the US’s biggest healthcare conglomerates. United Health’s stock fell 14%, Cigna’s 10% and CVS Health fell to a 12-year low last week.

Economic Updates

Inflation has not yet reached the Fed’s target of 2% and the economic outlook is still generally looking robust. Core consumer inflation, which excludes food and energy costs, rose by 0.3%, leaving the annual rate unchanged at 3.3% for the third month in a row. The November 2024 jobs report showed that nonfarm payrolls increased by 277,000 which was higher than the expected 214,000 and the Services PMI rose to its highest level in over three years at 58.5 (a number above 50 reflects growing demand). However, Manufacturing PMI fell to 48.30 points in December from 49.70 point in November. The result extends the poor momentum for US factory activity for a sixth month.

German year on year inflation rose from 2% in October to 2.2% (in September it had fallen to 1.6%). According to the Federal Statistical Office (“Destatis”), this was largely attributed to above average price increases for services.

Download the bulletin here.