Tactical Positioning

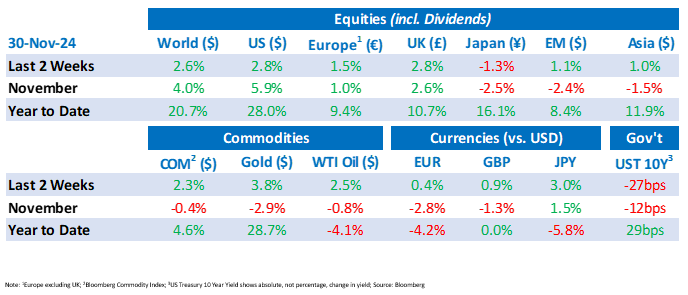

Market Moves

Trump on tariffs

The inflation outlook in the US is increasingly on investors’ minds, particularly given the statements from Donald Trump this week regarding tariffs. The President Elect announced that the US will impose 25% tariffs on all products from Mexico and Canada until they clamp down on drugs and migrants crossing the border into the US. He also announced an additional tariff on products from China of 10%, above any other tariffs, until it cracks down on Fentanyl smuggling. On the back of the announcement, the Mexican peso fell 1.8% last week and the Canadian dollar was the worst performing G10 currency falling 0.6%. The news comes just days after Trump hired Scott Bessent to be the next US Treasury Secretary, a move that was regarded positively by markets as it may signal a more measured tariff stance. Deutsche Bank’s economists estimate that US Core PCE inflation could increase to 3.7% if the tariffs are fully implemented. Before Trump’s election they were predicting 2.3% inflation in 2025.

Nvidia

Nvidia, the chipmaker at the heart of the AI boom, delivered stronger than expected earnings and revenues on 20th November and gave guidance for Q4 that was very slightly higher than consensus forecasts. The company’s share price has risen around 180% this year and it is currently the largest quoted company in the world with a market capitalisation of $3.48 trillion. The company’s guidance indicates that year-on-year revenues are likely to grow 70% in Q4 compared with 103% in the third quarter. Investors reacted to the news by focussing on the rate of growth slowing slightly and the share price fell 2.5%. This should, however, be viewed in the context of Nvidia’s staggering growth over the last two years.

Missiles in Russia and Ukraine

President Biden authorised Ukraine to use its US sourced ATACMS missiles to strike hundreds of miles inside Russia for the first time. In response President Putin signed a revision to Russia’s nuclear doctrine, allowing for an easing of the circumstances under which tactical (battlefield) nuclear weapons might be used. The news supported the price of gold which recovered part of the loss seen earlier in the month and briefly hit European equities before the market recovered with the German market finishing the month just below its all-time high.

Wake up and smell the coffee

The Confederation of British Industry (“CBI”) says that British businesses and employees were caught off guard by the £25bn tax rise announced in the budget in October and that the looming rise in employer National Insurance Contributions may weigh on growth. UK growth slowed in the second half of the year and the November flash Purchasing Managers’ index (“PMI”) fell from 51.8 in October to 49.9 in November. The reading is marginally below the neutral 50 level. However, it was the lowest in over a year and shows a loss of confidence post the budget. The Manufacturing index led the decline, with output contracting at the fastest pace for nine months. Attention will turn to the Bank of England who previously indicated a further rate cut in December is unlikely.

Economic Updates

US PMIs were strong and reduced expectations for the speed of interest rate cuts. US new home sales for October were 610k, their lowest since November 2022 and down 17.3%. Additionally in the US the weekly jobless claims fell to 213k similar to expectations of 215k.

Flash PMIs in Europe came in beneath expectations across the board leading to a fall in short-term interest rate expectations. The likelihood of a 50bps ECB rate cut in December increased to just under 50%.

10yr gilts fell, pushing yields higher, after the UK October Consumer Price Index (“CPI”) came in above expectations. Headline CPI rose to a six-month high of 2.3% vs 2.2% expected with core CPI at 3.3%.

Download the bulletin here.