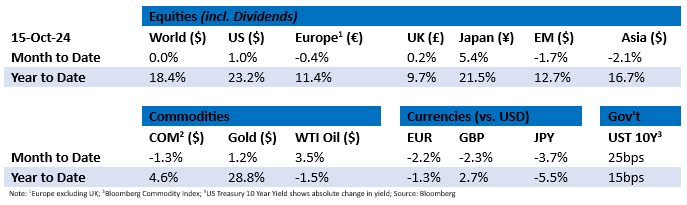

Tactical Positioning

Market Moves

Unrest in the Middle Eastern deepens

As the world marked the one-year anniversary of the 7th October Hamas attacks in Israel, geopolitical tensions in the Middle East showed no signs of abating. The conflict extended into southern Lebanon where Israel launched a ground attack on Hezbollah and carried out large-scale airstrikes in Beirut’s southern suburbs. The Biden Administration, having already called for a ceasefire, continued to condemn the attacks, calling for Israel to stop “absolutely” strikes on UN peacekeepers in Lebanon and halt any further movement into the region. The US has also imposed fresh sanctions aimed at cutting off financial support for Hamas, targeting both domestic and international backers of the group.

Perhaps unsurprisingly amid the escalation in military activities, the price of Brent Crude Oil experienced significant swings, including its biggest weekly gain since January 2024 (+8.4%) and its biggest daily increase (+5.0%) since October 2023. Prices fell back slightly to around $74bbl following the news that Israeli Prime Minister Netanyahu agreed to limit retaliatory strikes on Iran, focusing solely on military assets whilst avoiding their oil and nuclear infrastructure.

Losing your cool

The year-on-year headline US Consumer Price Index (“CPI”) figures for September came in marginally higher than expected, at 2.4%. ‘Core’ CPI, which excludes the more volatile effects of energy, food, alcohol and tobacco prices, also surprised to the upside, at 3.3% versus a predicted reading of 3.2%.

This higher than expected inflation coupled with a statement by Federal Reserve (“Fed”) Chair Jerome Powell that the Federal Open Market Committee was “not a committee that feels like it’s in a hurry to cut rates quickly” helped reduce the likelihood of a 50 basis points cut in rates at the Committee’s next meeting. Markets are now pricing in an 87% chance of a 25bp rate cut on 7th November.

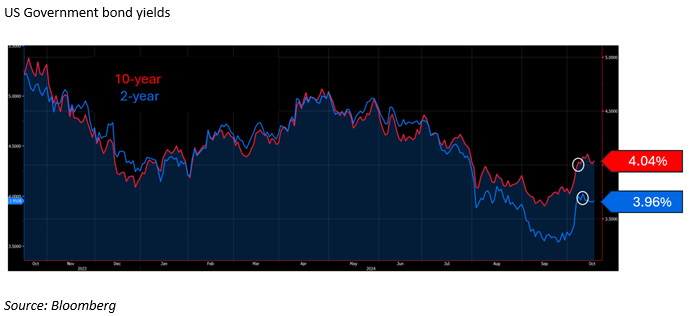

4% Treasury yields

Tensions in the Middle East and some knockout US payrolls data that point to the economy remaining strong led to the US 2-year and 10-year Treasury bonds seeing their yields rise to 4% for the first time since August.

The best 3 week run since 1965

Following a dismal 2023, when a broken real estate market, dwindling foreign investment and relentless government intervention led to the fall in the market, the announcement of a bumper stimulus package, including measures to cut banks’ required reserve ratio and a reduction in the 7-day reverse repo rate, led to the Hong Kong stock index posting its best performance since 2022 and its best 3 week run since 1965. However, after initially celebrating these government measures, volatility returned to Chinese markets following the Golden Week break with mainland stocks tumbling more than 7% amid uncertainty surrounding the scale of government stimulus. Enthusiasm diminished further as investors forecast that the country’s economic growth will be slightly under 5% this year.

Economic Updates

The US unemployment rate dropped to 4.1%, beating analysts’ forecast of 4.2% and signalling that the economy is in much better shape than anticipated. Additionally, the ISM Services data outperformed predictions, registering 54.9% compared with a projected 51.7%, marking the highest reading since February 2023 and surpassing nearly every economist’s estimate on Bloomberg. The stronger-than-expected data poured cold water on the likelihood of the Fed cutting rates as aggressively as previously thought. Investors, buoyed by the prospect of a more positive labour market, also helped US equities record their 46th high of 2024 so far.

The Q3 earnings season kicked off in the US with many large banks such as Wells Fargo, BlackRock and BNY Mellon posting decent results. Most notably JP Morgan, which announced quarterly profits of $12.9bn fuelled by gains in investment banking and rising interest payments which helped their share price jump 5% on the day. Elsewhere, Europe’s leading chipmaker ASML cited underwhelming earnings leading to a 15.6% fall in its share price, its worst daily fall since 1998.

Download the bulletin here.