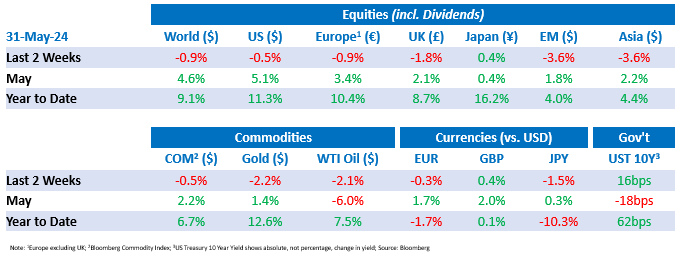

Tactical Positioning

In our last bulletin, we alluded to the depletion in US personal savings and the potential drag this may have on the economy, unless the Federal Reserve starts to cut interest rates. We also outlined how a decent earnings season from US corporates and ongoing excitement over the potential benefits of Artificial Intelligence has buoyed equity prices. Over the past fortnight, the rally in prices has paused. ‘Sell in May’ did not play out in 2024 but June could see a continuation of this pause and an increase in volatility brought on by mixed economic data. When market indices breach new highs as they did in May, it is normally a moment for reflection. We seem to be at this point now.

Market Moves

Time for a pause

Following a strong rise in markets in the first two weeks of the month, markets were subdued in the final fortnight as the earnings season in the US drew to a close and inflation numbers came in above central bank targets, even though the general trend is still downwards. Consequently, we still expect interest rates to be cut in the US and the UK and this week, the Eurozone is likely to be the first to move. Markets are indicating that it is highly likely that the European Central Bank will cut interest rates by 0.25%.

Chips selling like hot cakes

Nvidia again reached new highs after announcing impressive earnings, with sales up 262% in the first quarter of 2024. The stock’s rise was further fuelled by news that Elon Musk’s xAI startup has chosen to use Nvidia products to run its supercomputers. The share price has more than doubled since the start of this year and the company now has a market value of around $2.7 trillion, greater than the combined value of the 40 largest companies in the French stock market including names like LVMH, l’Oréal and TotalEnergies. Investors are of course concerned how much growth is already priced into the share price. The shares trade on a price to earnings multiple of 64 times the last twelve months earnings, so profits need to keep growing at a fast pace to justify the current price.

It was reported last week that the US is curbing sales of AI chips to the Middle East in an effort to prevent the technology from being transferred to China.

China’s growing, but is it enough

Although the IMF has recently raised its growth forecasts for China’s economy to 5% in 2024 and 4.5% in 2025, the economy still has many issues related to the slowdown in the property sector, weak consumer confidence and geopolitical concerns. Youth unemployment stood at 14.7% according to official data and this month a further 11.8m students are due to graduate. In our last Bulletin we highlighted the partial recovery in Chinese equity prices following the market setback in the previous six months. In the last two weeks Chinese equity indices have fallen slightly, impacted by US tariff increases and weak credit and inflation data. Although valuations of Chinese companies now look low, the market is volatile. The equity market is no higher than it was in 2007, despite four rallies along the way in which investors made near to or in excess of 100%. However, three of these rallies were followed by large falls (63% for the last one).

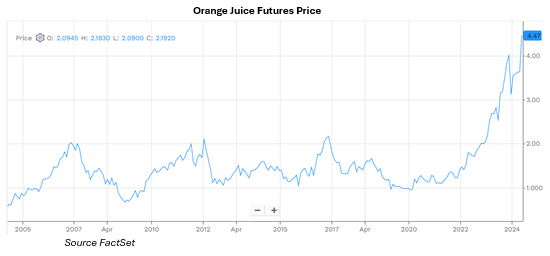

Orange juice futures squeezed higher

In general, commodity prices were softer during the fortnight. Ahead of a decision by OPEC to extend supply cuts, oil prices weakened partly owing to indications that demand in the US was weak. WTI and Brent crude finished slightly lower at $76.99 and $81.62, respectively, both experiencing their worst month in May.

This year’s unusual weather has significantly impacted many agricultural commodities. For example, bad weather and diseases in Brazil, the world largest exporter of oranges, has led to prices doubling over the last 12 months, reaching their all-time high.

Geopolitics and Elections

This year’s US election seems particularly newsworthy. The guilty verdict on all 34 felony counts of falsifying business records awarded to Donald Trump does not appear to have impacted his popularity. Of course, there are elections elsewhere in the world, most notably in India, the largest democracy in the world, which looks close to returning Narendra Modi for a third term whilst Mexico elected its first female president, Claudia Sheinbaum, a former mayor of Mexico City, who won about 60% of the vote last week. In the UK, Prime Minister Rishi Sunak has called a General Election on 4th July.

Economic Updates

US GDP was revised down to 1.3% annualized in the first quarter, below consensus expectations, reflecting a downward revision to consumption growth offset by upward revisions to housing and capex categories

Inflation data was mixed over the fortnight. In the Eurozone, the harmonised Consumer Price index rose 2.6% in May slightly higher than expected with core inflation increasing slightly to 2.9%, whilst in the UK core inflation slowed to 3.9%.

On Friday the US Department of Commerce published the Federal Reserve’s preferred inflation measure for April, the Personal Consumption Expenditures Price Index, which showed that inflation stayed at 2.7% in line with March’s reading and close to market expectations, but bonds reacted positively in expectation that US rates will be cut later this year.

Download the bulletin here.