TACTICAL POSITIONING

A reduction in the forecast speed and quantum of interest rate cuts in 2024 in the US and Europe does not seem to have upset equity investors. The pleasant surprise of the last 12 months is that higher interest rates have not derailed the global economy and shallow growth currently seems a more likely downside scenario than recession. Provided valuations do not rise too far from here and are supported by strong corporate earnings growth in 2024 we remain keen on equities. Shorter dated bonds also continue to look attractive as inflation slowly heads back below 3% in the largest global economies.

MARKET MOVES

Fed’s outlook prevails

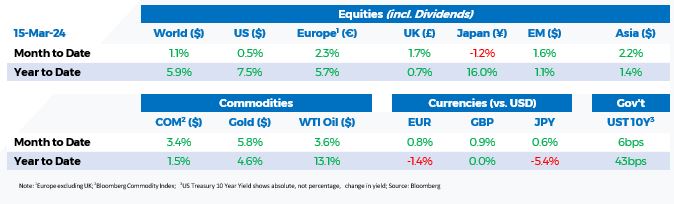

Financial markets are finally aligning with the Federal Reserve’s (“Fed”) outlook on US interest rates. Investors are moderating their expectations for rate cuts this year in response to economic data highlighting that although inflation has fallen significantly since last summer, reductions to the Fed’s target rate are likely to happen more slowly than markets had hoped. Initial expectations of over 150 basis points of cuts in interest rates during 2024 have now decreased to only 73 basis points and futures pricing suggest that there is less than a 10% chance of a cut in the US before June.

Although inflation has fallen significantly the latest numbers reflect a pause in that fall. US consumer prices rose 0.4% for a second consecutive month in February, driven primarily by higher gasoline and shelter costs. The annual level rose to 3.2% year-on-year from 3.1% in January. Similarly, producer prices surprised on the upside, rising 0.6% in February and 1.6% over 12 months.

Following the release of the data, Treasury yields increased, with the yield on US two-year Treasuries climbing to 4.71% from 4.63% over the fortnight, and the ten-year Treasury yield rose from 4.26% to 4.30%. Looking ahead, the Fed’s Open Market Committee meets this week and the Bank of England and Bank of Japan hold their respective policy meetings.

US equity market resilience

There was a notable inflow into US equity funds in the week to the 13th March. According to Barclays, investors added a record $56 billion, surpassing the previous peak of $53 billion set in March 2021,. Notably, a significant portion of these funds, totalling a record $22 billion, flowed into technology-focused funds. Investors are increasingly turning to tech stocks as a safe haven, displacing traditional defensive sectors like consumer staples and utilities. This shift may well be attributable to the robust balance sheets of the major tech companies.

According to the American Association of Individual Investors Investor Sentiment Survey, expectations of rising stock prices over the next six months, stands above its historical average for the 19th consecutive week, even though it decreased slightly last week.

UK spring budget

Chancellor of the Exchequer Jeremy Hunt unveiled a 2% reduction in National Insurance contributions for approximately 27 million workers, costing roughly £10 billion annually, alongside improvements to child benefit rules. Hunt plans to finance these initiatives in part by extending the windfall levy on energy firms and increasing taxes on vapes, tobacco, and non-economy class flights. The budget also includes the abolition of the ‘Non-dom’ tax regime, transitioning to taxing non-domiciled individuals residing in the UK for over four years on their overseas income—a measure anticipated to generate £2.7 billion annually. Aiming to boost investment in domestic businesses, the chancellor revealed plans for a new “British ISA,” providing savers an additional £5,000 tax-free allowance for investing in UK companies.

The budget brought few surprises. The pound hardly moved, while stocks continued to climb, although the increase has been at a slower pace than other markets this year. UK gilts remained stable, in contrast to the turmoil in bond markets following the unfunded tax cut proposals in the interim budget release in September 2022 under the previous Chancellor, Kwasi Kwarteng.

US security concerns prompt TikTok ban

The US House of Representatives passed a bill instructing ByteDance, the Chinese owner of TikTok, to divest its US assets within six months or face a ban. The bipartisan vote of 352-65 reflects mounting US national security concerns regarding China. The political climate in Washington, particularly amidst election sensitivities, increasingly supports the bill despite concerns over its impact on younger voters. Chinese stocks and Hong Kong shares fell, underscoring ongoing concerns regarding geopolitical risks and the deterioration of US-China relations.

ECONOMIC UPDATES

The European Central Bank has revised down its inflation forecasts for the Eurozone. Headline inflation of 2.3% is forecast for this year, 2.0% in 2025, and 1.9% in 2026, while core inflation of 2.6% is expected this year, 2.1% in 2025 and 2.0% in 2026.

In the US, the latest jobs report provided mixed signals. While February saw a robust addition of 275,000 jobs, surpassing expectations, January’s figures were revised down and the unemployment rate unexpectedly rose to 3.9%, its highest level in over two years, though still historically low. Additionally, average hourly earnings increased by 0.1%, below expectations and a sharp decline from January’s 0.5% increase.

British wages grew at 6.1% in the three months to January, however, falling inflation means that in real terms, pay increased by 2%, the fastest growth since September 2021.

Japan’s GDP was revised on the upside to a 0.4% expansion in the October-December period, above the initial estimate of a 0.4% contraction, intensifying speculation regarding a potential Bank of Japan policy tightening.

Download the bulletin here.